SHARE

SHARE

Analyzing a company's operating results is often the most important aspect of equity analysis. How well a company generates operating cash flow dictates how well it can satisfy the claims of creditors and create value for common shareholders. In order to assess this value creation, investors do well by analyzing a company's operating income, operating cash flow and operating margins.

Why Are Operating Margins Important?

Operating income is revenue less operating expenses for a given period of time, such as a quarter or year. Operating margin is a percentage figure usually given as operating income for some period of time divided by revenue for the same time period. Operating margin is the percentage of revenue that a company generates that can be used to pay the company's investors (both equity investors and debt investors) and the tax man. It is a key measure in analyzing a stock's value. Other things being equal, the higher the operating margin, the better. Using a percentage figure is also very useful for comparing companies against or analyzing the operating results of one company over various revenue scenarios.

Revenue can be derived in a number of ways, depending on the type of business. Similarly, operating expenses come from a variety of sources. Depending on the source, operating expenses "behave" in a variety of ways.

What is Operating Margin?

Operating margin is equal to operating income divided by revenue. Operating margin is a profitability ratio measuring revenue after covering operating and non-operating expenses of a business. Also referred to as return on sales, the operating income is the basis of how much of the generated sales is left when all operating expenses are paid off.

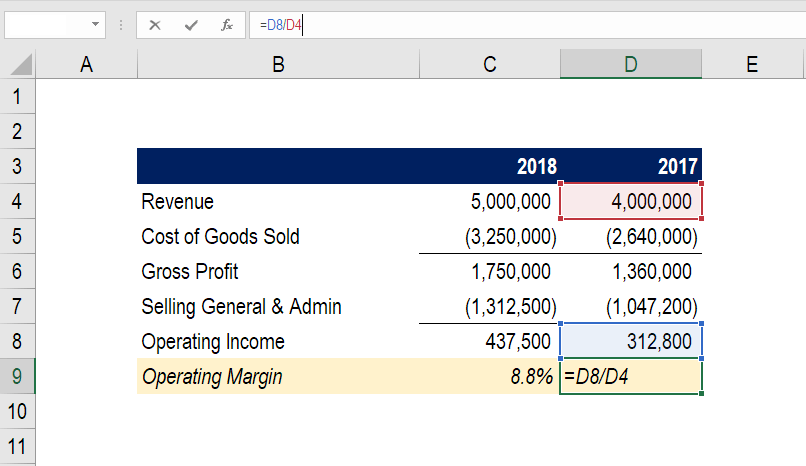

In the above example, you can clearly see how to arrive at the 2018 operating margin for this company. 2018 starts with Revenue of $5 million, less COGS of $3.25 million, resulting in Gross Profit of $1.75 million.

From there, another $1.3 million of Selling General & Administrative SG&A expenses are deducted, to arrive at Operating Income of $437,500.

By taking $437,500 and dividing it by $5.0 million you arrive at the operating margin of 8.8%.

What is the formula for Operating margin?

Operating Margin = Operating Income / Revenue X 100

Another example:

DT Clinton Manufacturing company reported on its 2015 annual income statement a total of $125 million in sales revenue. Operating income before tax netted to $45 million after deducting all operating expenses for the year. As a result, an operating margin of 36% was generated after deducting all the operational expenses of $80 million. Hence, for every dollar in sales achieved, $0.36 cents is retained as operating profit.

What is Operating Income?

Operating income is the profit of a business after all operating expenses are deducted from sales receipts or revenue. It represents how much a company is making from its core operations, not including other income sources not directly related to its main business activities. It differs from net income in that it does not include the expenses of taxes and interest.

This gives an idea for investors and creditors if a company’s core business is profitable or not, before considering non-operating items.

What is Sales Revenue?

Sales revenue or net sales is the monetary amount obtained from selling goods and services to business customers excluding the merchandise returned and the allowances/discounts offered to them. This can be realized either as cash sales or credit sales.

Why is Profit Margin important in business?

A business that is capable of generating operating profit rather than operating at a loss is a positive sign for potential investors and existing creditors. This means that the company’s operating margin creates value for shareholders and continuous loan servicing for lenders. The higher the margin that a company has, the less financial risk it has as compared to a lower ratio.

Continued increases in profit margin over time shows that profitability is improving. This may either be attributed to an efficient control of operating costs or other factors that influence revenue build-ups such as pricing, marketing, and increase in customer demand.

The drawbacks of looking at operating margin/profit

Operating profit is an accounting metric, and therefore not necessarily an indicator of economic value or cash flow. Profit includes several non-cash expenses such as depreciation and amortization, stock-based compensation, and other items. Conversely, it doesn’t include capital expenditures and changes in working capital.

In conjunction, these various items are that included and excluded could cause cash flow (the ultimate driver of value for a business) to be very different (higher or lower) than operating profit.

To learn more, read all about business valuation.

Fixed and Variable Costs

Analysts often characterize expenses as either "fixed" or "variable" in nature. A fixed cost is a cost that remains relatively steady as business activity and revenue change. A rent expense is an example. If a company leases or rents a property, it usually pays a set amount each month or quarter. This amount does not change regardless of whether business is good or bad at the time. By contrast, a variable cost is one that changes as business activity changes. One example is the cost of buying raw materials for a manufacturing operation. Manufacturing companies must buy more raw materials when business speeds up; therefore, the cost of buying raw materials increases as revenue increases.

Analyzing a company's mix of fixed and variable costs, called a company's operating leverage, is often important in analyzing operating margins and cash flows. When revenue increases, the operating margins of companies that are fixed-cost intensive have the potential to increase at a faster rate than that of less fixed-cost-intensive companies (the reverse is also true). Because equity analysis involves projecting future operating results, understanding the relative importance of fixed costs is vital. Analysts must understand how operating margins will change in the future given certain revenue growth assumptions.

Factoring in the Cost of Goods

A special and important form of expense is cost of goods sold (COGS). For companies selling products that they manufacture, add value to or simply distribute, the cost of products sold is accounted for using inventory calculations. The basic formula for COGS is:

COGS = BI + P - EI

Where:

|

COGS strives to measure the cost of inventory sold in a period; the actual amount incurred to buy inventory might be significantly higher or lower. By netting out beginning and ending inventory, companies try to measure the cost of the actual volume of product sold during the period. Also note that a significant amount of overhead costs—such as the power bill for a manufacturing plant—is often embodied in inventory amounts and therefore in COGS itself.

Revenue less COGS is known as gross profit and it is a key element of operating income. Gross profit measures the amount of profit generated before general overhead costs that cannot be inventoried, like selling, general and administrative (SG&A) costs. SG&A costs might include such items as administrative staff salaries or costs to maintain a stock market listing.

Gross profit divided by revenue is a percentage value known as gross margin. Analyzing gross margin is paramount in equity analysis projects because COGS is often the most significant expense element for a company, and is found on their income statement. Analysts often look at gross margin when comparing companies or assessing the performance of a single company in a historical context.

Other Considerations

Investors should also understand the difference between cash expenses and non-cash expenses when analyzing operating results. A non-cash expense is an operating expense on the income statement that does not require cash outlay. An example is depreciation expense. According to generally accepted accounting principles (GAAP), when a business buys a long-term asset (such as heavy equipment), the amount spent to buy that asset is not expensed in the same way as rent expense or raw materials cost might be.

Instead, the cost is spread out over the useful life of the equipment, and therefore a small amount of the overall cost is allocated to the income statement over a number of years in the form of depreciation expense, even though no further cash outlay has occurred. Note that non-cash expenses are often allocated to other expense lines in the income statement. A good way to grasp the effect of non-cash expenses is to look carefully at the operating section of the statement of cash flows.

It is largely because of non-cash expenses that operating income differs from operating cash flow. Investors are wise to consider the proportion of operating income that is attributable to non-cash expenses. Analysts often calculate earnings before interest, taxes, depreciation and amortization (EBITDA) to measure cash-based operating income. Because it excludes non-cash expenses, EBITDA may better measure the amount of cash flow generated from operations that is available for investors, than operating income. After all, dividends must be paid from cash, not income. Similar to gross margin and operating margin, analysts use EBITDA to calculate EBITDA margin and they use this figure to do company comparisons and historical company analyses.

The Bottom Line

In order to properly assess most equities, investors must grasp the issuer's ability to generate cash flow from operations. It is therefore vital to understand the concepts of operating income and EBITDA. As with most aspects of financial analysis, numerical comparisons can tell more about a company than the actual financial parameters. By calculating margins, investors can better measure a company's ability to generate operating income in competitive and historical contexts.

Operating Profit Margin Ratio

The operating profit margin ratio indicates how much profit a company makes after paying for variable costs of production such as wages, raw materials, etc. It is also expressed as a percentage of sales and then shows the efficiency of a company controlling the costs and expenses associated with business operations. Furthermore, it is the return achieved from standard operations and does not include unique or one time transactions. Terms used to describe operating profit margin ratios this include the following:

Operating Profit Margin Formula

In order to calculate the operating profit margin ratio formula, simply use the following formula:

Operating profit margin = Operating income ÷ Total revenue

(NOTE: Want the Pricing for Profit Inspection Guide? It walks you through a step-by-step guide to maximizing your profits on each side. Get it here!)

Operating Profit Margin Calculation

The operating profit margin calculations are easily performed, including the following example.

Operating Income = gross profit – operating expenses

For example, a company has $1,000,000 in sales; $500,000 in cost of goods sold; and $225,000 in operating costs. In conclusion, operating profit margin = (1,000,000 – 500,000 – 225,000)= $275,000 / 1,000,000 = 27.5%

Operating Margin Ratio

Operating margin ratio or return on sales ratio is the ratio of operating income of a business to its revenue. It is profitability ratio showing operating income as a percentage of revenue.

Formula

Operating margin ratio is calculated by the following formula:

Operating income is same as earnings before interest and tax (EBIT). Both operating income and revenue figures can be obtained from the income statement of a business.

Analysis

Operating margin ratio of 9% means that a net profit of $0.09 is made on each dollar of sales. Thus a higher value of operating margin ratio is favorable which indicates that more proportion of revenue is converted to operating income. An increase in operating margin ratio overtime means that the profitability is improving. It is also important to compare the gross margin ratio of a business to the average gross profit margin of the industry. In general, a business which is more efficient is controlling its overall costs will have higher operating margin ratio.

Examples

Example 1: Determine the operating margin ratio of Company α given that its sales are $928,300 and its operating income is $113,200 for the month. What is the performance of the company compared to its industry which has average operating margin ratio of 10%?

Solution

Operating margin ratio = $113,200 / $928,300 ≈ 0.12 = 12%

The company is more profitable than an average firm in its industry.

Operating margin ratio = $113,200 / $928,300 ≈ 0.12 = 12%

The company is more profitable than an average firm in its industry.

Example 2: Calculate operating margin ratio from the following information:

Solution

Step 1: Revenue = $34,390 + $42,030 = $76,420

Step 2: Operating Income = $42,030 − $37,200 = $4,830

Step 3: Operating Margin Ratio = $4,830 / $76,420 ≈ 0.063 or 6.3%

Step 1: Revenue = $34,390 + $42,030 = $76,420

Step 2: Operating Income = $42,030 − $37,200 = $4,830

Step 3: Operating Margin Ratio = $4,830 / $76,420 ≈ 0.063 or 6.3%

A:

Typically, an operating profit margin of a company should be compared to its industry or a benchmark index like the S&P 500. For example, the average operating profit margin for the S&P was roughly 11% for 2017. A company that has an operating profit margin higher than 11% would have outperformed the overall market. However, it's important to take into consideration that average profit margins vary significantly between industries.

Operating profit margin is one of the key profitability ratios that investors and analysts consider when evaluating a company. Operating margin is considered to be a good indicator of how efficiently a company manages expenses because it reveals the amount of revenue returned to a company once it has covered virtually all of both its fixed and variable expenses except for taxes and interest.

What Does Operating Profit Margin Tell Investors and Business Owners

The operating profit margin informs both business owners and investors about a company's ability to turn a dollar of revenue into a dollar of profit after accounting for all the expenses required to run the business. This profitability metric is calculated by dividing the company's operating income by its total revenue. There are two components that go into calculating operating profit margin: revenue and operating profit.

Revenue is the top line on a company's income statement. Revenue, which is sometimes referred to as net sales, reflects the total amount of income generated by the sale of goods or services. Revenue refers only to the positive cash flow directly attributable to primary operations.

Operating profit sits further down the income statement and is derived from its predecessor, gross profit. Gross profit is revenue minus all the expenses associated with the production of items for sale, called cost of goods sold (COGS). Since gross profit is a rather simplistic view of a company's profitability, operating profit takes it one step further by subtracting all overhead, administrative and operational expenses from gross profit. Any expense necessary to keep a business running is included, such as rent, utilities, payroll, employee benefits, and insurance premiums.

How Operating Profit Margin Is Calculated

By dividing operating profit by total revenue, the operating profit margin becomes a more refined metric. Operating profit is reported in dollars, whereas its corresponding profit margin is reported as a percentage of each revenue dollar. The formula is as follows:

One of the best ways to evaluate a company's operational efficiency is to view the company's operating margin as it changes over time. Rising operating margins show a company that is managing its costs and increasing its profits. Margins above the industry average or the overall market indicate financial efficiency and stability. However, margins below the industry average might indicate financial vulnerability to an economic downturn or financial distress if a trend develops.

Operating profit margins vary greatly across different industries and sectors. For example, average operating margins in the retail clothing industry run lower than the average operating profit margins in the telecommunications sector. Large, national-chain retailers can function with lower margins due to the massive volume of their sales. Conversely, small, independent businesses need higher margins in order to cover costs and still make a profit.

Example of Operating Profit Margin

Apple Inc. (AAPL)

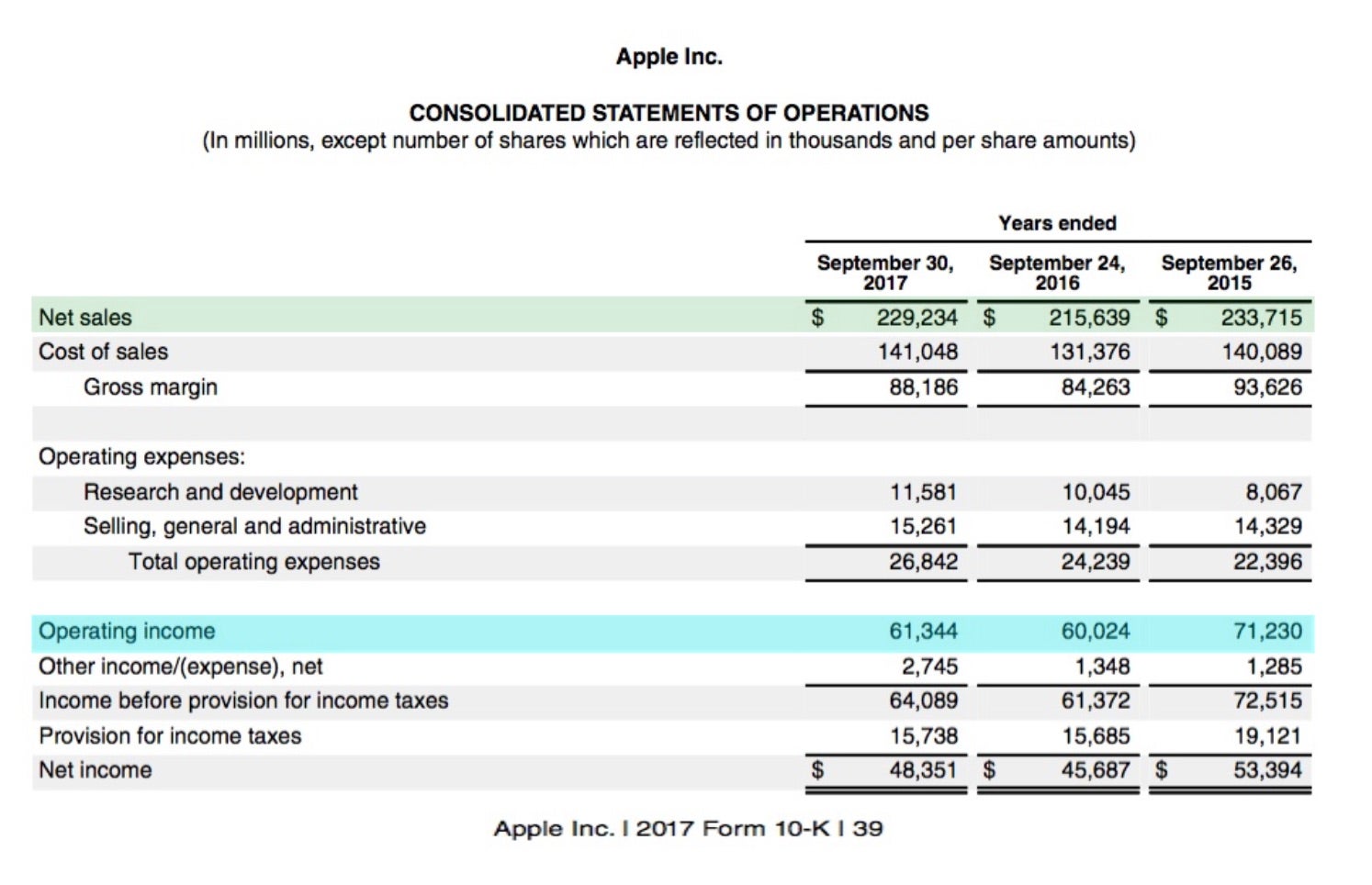

Apple reported an operating income number of roughly $61 billion (highlighted in blue) for the fiscal year ended September 30, 2017, as shown in its consolidated 10K statement below. Apple's total sales or revenue was $229 billion for the same period.

As a result, Apple's operating profit margin for 2017 was 26.6% ($61/$229). However, the number by itself doesn't tell us much until we compare it to prior years.

- 2017 Operating margin = 26.6% ($61/$229).

- 2016 Operating margin = 27.9% ($60/$215).

- 2015 Operating margin = 30.0% ($71/$234).

By analyzing multiple years, we can see that a trend has developed over the past three years where Apple's operating margins have fallen by 3.4% since 2015. Analysis of a company's operating margin should focus on how it compares to its industry average and its closest competitors, along with whether the trend of the company's margin is generally increasing or decreasing year by year.

The Bottom Line

A consistently healthy bottom line depends on rising operating profits over time. Companies use operating profit margin not only to spot trends in growth, but also to pinpoint unnecessary expenses to determine where cost-cutting measures can boost their bottom line. To gauge a company's performance relative to its peers, investors can compare its finances to other companies within the same industry. However, this metric is also useful in the development of an effective business strategy as well as serving as a comparative metric for investors.

For more financial analysis, please read "How the Income Statement and Balance Sheet Differ?"

We find accounting profitability exclusively on the income statement, which teases out four levels of profit or profit margins: gross profit, operating profit, pre-tax profit and net profit.

Conceptually, the income statement assumes the following sequence: A company takes in sales revenue, then pays direct costs of the product of service. What’s left is gross margin. Then it pays indirect costs like company headquarters, advertising, and R&D. What’s left is operating margin. Then it pays interest on debt and adds or subtracts any unusual charges or inflows unrelated to the company’s main business with pre-tax margin left over. Then it pays taxes, leaving net margin, also known as net income, which is the very bottom line.

Three logistical points before getting to the math:

- Semantically, “profit,” “income,” and “margin,” are all used interchangeably, although margin usually refers to a percentage, whereas profit and income exclusively denote monetary amounts.

- When talking about profitability analysis, percentages are more frequently used than raw numbers because they enable comparison among companies and across a company’s own time horizon.

- Finding margin numbers is easy these days. You can never go wrong pulling the actual numbers from a company’s filings, but many of financial websites have them pre-calculated. Be careful though! Auto-calculating tools have been known to goof on rare occasion.

The major profit margins all compare some level of residual (leftover) profit to sales. For instance, a 42% gross margin means that for every $100 in revenue, the company pays $58 in costs directly connected to producing the product or service, leaving $42 as gross profit.

The Major Margins

Now we’ll see how WD-40 Co.’s (WDFC) 2016 margins look (data from page F-3 on the 2016 10-K):

- Gross profit margin: $214.4m / $380.7m = 56%

- Operating profit margin: $71.3m / $380.7m = 19%

- Pre-tax profit margin: $72.8m / $380.7m = 19%

- Net profit margin: $52.6m / $380.7m = 14%

How should we feel about these numbers? The quick answer is that these numbers show a strong business, at least by most standards.

For example, data from New York University finance professor Aswath Damodaran’s website indicates that as of January 2017, the average U.S. public company industry net profit margin was just 6%, with operating margin around 10%, well below WD-40’s. WD-40 (named for chemist Norm Larsen’s 40th attempt at a water displacement formula to coat intercontinental ballistic missiles) has a dominant market position with strong pricing power. Its products are cheap enough in the first place that consumers aren’t particularly motivated to save a few dimes on a generic substitute.

Peer comparisons are a bit tricky because WD-40 is really the only pure-play publicly traded lubricant company, which, in fairness, is a testament to the company’s dominance. Auto-populated investing websites will list industrial chemical companies like Dow and E.I. duPont as comparables or competitors; they’re much closer kin than, say, biotechs or railroads, but they’re not perfect yardsticks. And because WD-40 has held its competitive ground since it was founded in 1953 (long enough ago that if it were a person, WD-40 would already be collecting Social Security), we don’t have compelling evidence to believe that its margins will mean-revert to industrial chemical averages.

Margin of Error: Caveats About Using Income Statement Profit Margins

- Quoting profits in raw dollar (or other currency) terms and using percentage terms both come with problems. The raw currency number accurately depicts aggregate profit, but it is a clunky tool for comparison. Percentages accurately show per-unit profitability, but say nothing about units sold. Returning to professor Damodaran’s data for an example, U.S. grocery stores have a 1.89% average net margin, meaning they net just $1.89 for every $100 of merchandise sold. That sounds wimpy, but the end game is cash in the bank, and supermarkets can make up for their low margin with high volume.

- The income statement tells us very little about capital structure. A company could issue a slug of debt or sell a bunch of shares to get cash to boost sales and profits, but profits alone don’t reveal whether this was a value-adding move for shareholders.

- Income statement numbers are based on accrual accounting, and are thereby more subject to manipulation than cash flows.

- The income statement (at least under many countries’ accounting rules) doesn’t fairly capture the economics of all industries. For Real Estate Investment Trusts (REITs), for example, most analysts massage net income into a measure called funds from operations (FFO) that undoes an accrual called depreciation. Plug-and-chug types may miss these nuances if not careful.

The key limitation in divining profitability solely from the income statement is caveat (2) above: The income statement tells us only part of the profit picture – the inflows and immediate expenses used to generate those inflows – but not about the capital resources, like asset or equity base, required. For that, we’ll have to look at the balance sheet (and another lesson).

EBITDA: Earnings Before Bad Stuff?

One profitability number you won’t see on the income statement, but will see in a lot of other places (especially the haunts of investment bankers and Wall Street analysts) is earnings before interest, taxes, depreciation, and amortization, or EBITDA.

EBITDA, which would fit in between gross profit and operating profit were it to be on the income statement, is simply operating profit (or earnings before interest and taxes; i.e., EBIT) with the previously subtracted accrual charges of depreciation (the “D”) and amortization (the “A”) added back in.

What’s the point?

EBITDA came into vogue among 1980s investment bankers looking for a quick and dirty cash flow proxy (the Statement of Cash Flows wasn’t the norm until 1988). EBITDA caught a second wave in the tech-crazed 1990s, when earlier and earlier-stage companies saw IPO and acquisition interest.

Acquisition types like to express prices in terms of multiples of profit or cash flow: 20 times earnings, 12 times EBIT, etc.. But many hot companies of this generation didn’t have positive net income (so P/E multiples were out), and often had losses at the pre-tax and operating levels, too. Undeterred, bankers and sell-side Wall Street analysts went up and then off the income statement to produce a number more likely to be positive and easily comparable for early stage companies: EBITDA.

The value of EBITDA depends on its use. The metric leaves out a number of relevant expenses (“earnings before bad stuff” is one nickname), and the metric arguably sees too much use as a proxy for cash flow. Such cases suggest either poor understanding or even a shade of manipulativeness on behalf of the user.

Apparently, WD-40 didn’t get the memo about EBITDA’s warts: Page 21 of its 2016 proxy proclaims that EBITDA is both the #1 and #2 metric (per-segment, and consolidated, respectively) in determining management’s bonus. Fortunately, management appears to be well-behaved and effective, but an EBITDA target is considered risky because it leaves the door open for management to borrow vast sums of money to juice sales and EBITDA: The metric is blind to interest expense, debt outstanding, and capital expenditures.

Framing the Margins

Gross Profit Margin: Start with sales and take out costs directly related to creating or providing the product or service like raw materials, labor, and so on – typically bundled as "cost of goods sold,” “cost of products sold,” or “cost of sales” on the income statement – and you get gross margin. Done on a per-product basis, gross margin is most useful for a company analyzing its product suite (though this data isn’t shared with the public), but aggregate gross margin does show a company’s rawest profitability picture.

Companies have some discretion about whether to include certain expenses in cost of goods sold (COGS) or “selling, general and administrative” (SG&A) expenses, one expense line down the income statement. WD-40, for example, sticks some costs in SG&A that others stick in COGS. For analyzing or comparing WD-40’s operating margins, this is a non-event because the same costs are included; order doesn’t matter. But an investor making an investment decision solely based on gross margin analysis could mistakenly conclude that WD-40 is better than it really is. Fortunately, the situation is well-disclosed, at least to people who take the time to read the notes following financial statements (disclosures like these typically follow the actual financial statements on forms 10-K or 10-Q):

Note that our gross profit and gross margin may not be comparable to those of other consumer product companies, since some of these companies include all costs related to distribution of their products in cost of products sold, whereas we exclude the portion associated with amounts paid to third parties for shipment to our customers from our distribution centers and contract manufacturers and include these costs in selling, general and administrative expenses. These costs totaled $15.8 million and $16.2 million for the fiscal years ended August 31, 2015 and 2014, respectively.

Operating Profit Margin: By subtracting selling, general and administrative, or operating expenses, from a company's gross profit number, we get operating income, also known as earnings before interest and taxes, or EBIT.

Operating profit is a big deal, sometimes more so than net income. All the costs of actually providing the product or service have been taken out, resulting in an income figure that’s available to pay both types of capital providers to the business (debt and equity holders), as well as the tax department. Operating profit is profit from a company’s main, ongoing operations; oddball accounting adjustments like income from discontinued operations and extraordinary items are accounted for below this line (they do get bundled into pre-tax income, discussed below). Accordingly, operating income feels purer and less prone to weird accounting-related fluctuations to analysts than net income. Finally, because operating income is conceptually “owned” by both debt and equity holders (whereas net income is just for equity holders, interest expense having been paid), it’s frequently used by bankers and analysts to value an entire company for potential buyouts.

Pretax Profit Margin: Take operating income and subtract interest expense while adding any interest income, adjust for non-recurring items like gains or losses from discontinued operations, and you’ve got pre-tax profit, or earnings before taxes, or EBT. Note that for whatever reason, pre-tax profit is relatively more popular among UK analysts, whereas operating income reigns supreme across the Atlantic.

Net Profit Margin: If someone asks you, “What’s your company’s profit margin?” they’re most likely asking about net profit margin, or a company’s bottom line after all other expenses, including taxes and one-off oddities, have been taken out of revenue. If you’re a stockholder net income is what you “own,” at least conceptually. If it feels like everybody and his brother gets paid before you do, it’s true. Unlike everybody else, who gets paid a set amount, you as a shareholder get whatever is left, be it much or little. Technically, you seldom actually get it: the company may choose to reinvest that profit, stockpile it, squander it, buy back shares, or pay shareholders a dividend (in which case you actually would get it, or at least some of it). But wherever it goes, net profit, as long as it’s not squandered, adds value to shareholders like us, which is why we bought the stock in the first place.

No comments:

Post a Comment